The payment service enables transfers eligible for instant payment to be executed in just a few seconds, on any day of the year, any time of day. This means that transfers initiated over the weekend or after banking hours will also be executed instantly.

FOR PRIVATE INDIVIDUALS

FOR SMALL BUSINESSES AND CORPORATE CLIENTS

Where can I find additional information on instant payment?

You can find additional details on this website:

You can pay simply, even with a QR code, at merchants that provide the option, since

From 1 September 2024, UniCredit Bank’s mBanking and mBanking Business services also include qvik, an instant transfer initiated with a single data entry solution.

Starting from 06.03.2024, the request-to-pay service is available at UniCredit Bank

Request-to-pay is a standardised message sent by the beneficiary to the payer to initiate a payment in the domestic payment system for the settlement and execution of an instant payment transfer order. In other words, a request-to-pay order is an instant credit transfer order in HUF, prepared by the beneficiary and sent to the payer, which is received by through the electronic banking channel used by the payer. The transaction requires the explicit consent of the payer.

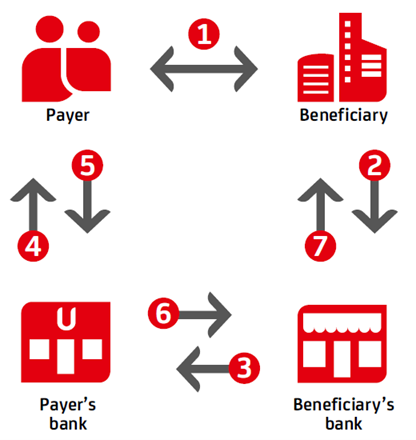

The request-to-pay process:

- Agreement on the payment method and collection of account information (name + account number or secondary identifier) from the Payer.

- The Beneficiary creates a payment request, providing the payer and transaction detail.

- The Beneficiary’s bank forwards the request-to-pay order to the payer's bank (if the payer is not an intra-bank) via GIROINSTANT clearing system.

- The Payer's bank notifies the Payer of the receipt of the request (at the same time confirming to the Beneficiary's bank that the request has been successfully received).

- The Payer may approve the request before the expiry date, initiating an instant payment, but may also reject it.

- A positive response to the payment request is received by the Beneficiary's bank in the form of an instant payment (in case of rejection, a reject confirmation will be sent).

- The Beneficiary's bank credits the amount to the Beneficiary's account and informs the Beneficiary that the request has been successfully fulfilled (in case of rejection, the beneficiary will be notified of the rejection).