Information about the repayment moratorium

INFORMATION ON AGRARIAN MORATORIUM

Dear Client,

Please be informed that the Government of Hungary provides a moratorium for agrarian enterprises from 1. September 2022 until 31. December 2023.

The payment moratorium shall apply to loans already disbursed based on agreements existing on 31. August 2022.

A borrower can take part in the moratorium if

- the ratio of his/her 2021 annual net turnover – calculated without the cost of goods sold – deriving from the sectors of crop and animal production, hunting and related service activities, forestry and logging, fishing compared to the 2021 total annual net turnover is at least 50% or

- the purpose of his/her loan serves any of the sectors in section 1).

If you intend to use the payment moratorium You are required to make a declaration until 15. September 2022. You can do this in person in our branch office or on-line (via e-mail, electronic channel).

Submission by post is not acceptable.

Failure to meet the deadline for making the declaration renders the declaration null, and void.

We shall provide You with detailed information on our website regarding the conditions and method of making the declaration.

Yours Sincerely,

UniCredit Bank Hungary Zrt.

Additional information concerning the payment moratorium

It is important to note that the payment moratorium (or grace period for payment) does not mean that the client's payment obligation ceases, it is only postponed.

Interests and fees not paid during the moratorium period are not capitalised and do not accrue interest either during the moratorium or at the end of the moratorium, and must be paid in equal instalments with the remaining repayment instalments due over the remaining term. As a result, the total term of the loan increases, the maturity of the loan is extended by a higher extent than the period under the moratorium, and thus the total amount payable over the entire term also increases.

Dear Client!

Please note that the legislation* on the loan repayment moratorium has been amended by the legislator.

The moratorium has been extended for all eligible clients until 31 December 2022, upon the condition that that only those are entitled to remain in the payment moratorium whose credit was also covered by the moratorium in June. However, after that date, i.e. from 1 August, only clients will be able to benefit from the moratorium until 31 July 2022 the latest who requested this option.

If you are still entitled to the repayment moratorium from 1 August 2022 and wish to continue to benefit from this option, you must make a declaration to this end to our bank until 31 July 2022. After that date, a declaration to employ the moratorium will not be accepted.

If your loan is currently covered by the moratorium, it will automatically remain so according to the applicable law until 31 July 2022. (Unless you notify our bank about your intent to repay your loan).

The moratorium will expire on 31 July 2022 for those who are not eligible for the extension or do not wish to continue from 1 August 2022, i.e. do not apply for the extension. In these cases you have nothing else to do but to continue repaying your loan with the instalment due in August 2022.

You can withdraw from the moratorium at any time by clicking on the “Declaration on notification about repayment under the original contractual terms” form to be submitted to our bank. If you opt out of the moratorium, you will not be able to reverse this decision later.

Additional information concerning the payment moratorium

It is important to note that the payment moratorium (or grace period for payment) does not mean that the client's payment obligation ceases, it is only postponed.

Interests and fees not paid during the moratorium period are not capitalised and do not accrue interest either during the moratorium or at the end of the moratorium, and must be paid in equal instalments with the remaining repayment instalments due over the remaining term. As a result, the total term of the loan increases, the maturity of the loan is extended by a higher extent than the period under the moratorium, and thus the total amount payable over the entire term also increases.

In the case of retail loans/credit lines, our bank offers its clients the opportunity of paying (prepaying) all or part of the interest, fees and charges they have accumulated during the moratorium, free of charge.

However, the extended term after opting out of the moratorium does not automatically revert to the original contractual term if the total debt accumulated during the moratorium is repaid early. The amount prepaid reduces the amount of the monthly repayment instalment payable. In the event of the full repayment of the debt accumulated during the moratorium, naturally, clients may request the reduction of the loan term (even requesting the duration set out in the original loan agreement).

In order to reduce the extended term, customers can undertake monthly repayments higher than the post-moratorium repayment instalments. This is conditional on compliance with the legal requirements for the payment-to-income ratio, even in case of higher repayment instalments.

No bank fees are charged for the above agreement amendments requested by our clients until 31 December 2022. It is important to note that the notary public fee for mortgage loans is not a bank fee and, as such, in the case of an agreement amendment, the client is required to pay this cost to the notary public.

It is of paramount importance for our Bank that our clients are able to assess the future impact of the payment moratorium on debt service, that the majority of debtors currently under the moratorium resume repayment, and that only those who genuinely need the safety net of the moratorium take advantage of the extension.

With the intent of helping our clients make the above prudent and conscious decisions, the following example illustrates the financial impact of participating in the moratorium for an average mortgage loan.

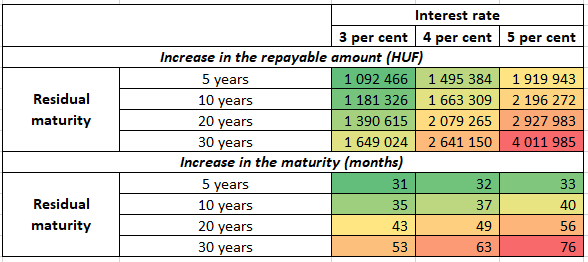

The impact of the payment moratorium between March 2020 and June 2022 on the total amount repayable and the term in case of a HUF 15 million housing loan

Comment: The extension of the loan term also includes the 27 months under the moratorium. Source: MNB.

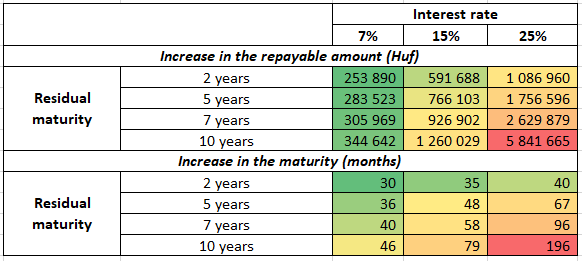

The impact of a payment moratorium between March 2020 and June 2022 on the total amount repayable and the term in case of a HUF 1.5 million personal loan

Comment: The extension of the loan term also includes the 27 months under the moratorium. Source: MNB.

Based on the above, the total amount to be repaid increases in excess of 10% for more than half of housing loan borrowers and in excess of 40% for more than half of personal loan borrowers.

Source: Magyar Nemzeti Bank: Report on the impact of the moratorium

1st July, 2022

Yours sincerely,

UniCredit Bank Hungary Zrt.

* Government Decree 536/2021 (IX. 15.) on amending Government Decree 637/2020 (XII. 22.) on the introduction of special emergency rules for the loan repayment moratorium

Information for private individuals

Please note that the legislation on the loan repayment moratorium has been amended by the legislator.

The moratorium has been extended for all eligible clients until 31 October 2021, upon the condition that that only those are entitled to remain in the payment moratorium whose credit was also covered by the moratorium in September. However, after that date, i.e. from 1 November, only clients in priority social groups will be able to benefit from the moratorium until 30 June 2022 the latest who requested this option.

Between 1 November 2021 and 30 June 2022, the moratorium is open to those private individuals who

- receive an old-age pension or a survivors' pension,

- maintain a biological or an adopted child under the age of 25,

- maintain a biological or adopted disabled child under the age of 25,

- are expecting a child and have passed the 12th week of pregnancy,

- are jobseekers,

- are public employees, and

- whose household income has decreased permanently after 18 March 2020.

The extended credit moratorium is open to businesses whose net turnover from business activities has decreased by at least 25 percent in the last 18 months preceding the application and the business has not entered into a new contract for a preferential loan or credit for economic recovery between 18 March 2020 and the date of application.

The extension of the repayment moratorium is not available to consumers with credit agreements secured by securities (lombard loans), loan agreements secured by chattel mortgage and financial leasing agreements for the purposes of using a vehicle.

To employ the moratorium from 1 November 2021, you must have used the moratorium in September 2021 as well.

If, based on the conditions referred to above, you are entitled to a further extension of the repayment moratorium and you wish to continue to benefit from it after 31 October 2021, you must notify our bank in a declaration between 1 October 2021 and 31 October 2021. You can only submit your declaration using the form stipulated by law:

- online in our eBanking internet banking system, using the form available with your specific loan, or

- in person in our branches by filling out the Declaration on the use of the payment moratorium form.

If your loan is currently covered by the moratorium, it will automatically remain so according to the applicable law until 31 October 2021. (Unless you notify our bank about your intent to repay your loan).

The moratorium will end on 31 October 2021 for those who are not eligible for an extension or do not wish to continue from 1 November 2021, i.e. do not apply for an extension. In these cases you have nothing else to do but to continue repaying your loan with the instalment due in November 2021.

You can withdraw from the moratorium at any time by clicking on the “Declaration on notification about repayment under the original contractual terms” form to be submitted to our bank. If you opt out of the moratorium, you will not be able to reverse this decision later.

1 October, 2021

Yours sincerely,

UniCredit Bank Hungary Zrt.

* Government Decree 536/2021 (IX. 15.) on amending Government Decree 637/2020 (XII. 22.) on the introduction of special emergency rules for the loan repayment moratorium

Information for companies

Dear Client!

Please be informed that the Government of Hungary has extended the credit moratorium until 30 June 2022.

The extended credit moratorium is open to businesses whose net turnover from business activities has decreased by at least 25 percent in the last 18 months preceding the application and the business has not entered into a new contract for a preferential loan or credit for economic recovery between 18 March 2020 and the date of application.

The conditions for employing the credit moratorium have been changed so that if your business is currently (in the month of September 2021) making use of the credit moratorium, you must declare between 1 October and 31 October 2021 whether you wish to continue using the moratorium (from 1 November 2021). You can do this either in person at our branch or online.

The 3rd phase of the moratorium is therefore open to companies that

- were covered by the moratorium on 30 September, 2021,

- provided the Bank with a declaration between 1 October and 31 October, 2021 of the fact

- that the company's net turnover from its business activities has decreased by at least 25% in the last 18 months preceding the submission of the application and the company declares that it has the supporting documents or other conclusive evidences to justify this, and

- the company has not entered into a new contract for a preferential loan or credit for economic recovery between 18 March 2020 and the date of application.

Only those businesses may enter the 3rd phase that have a net turnover from their business activity. Condominiums, foundations, churches and associations can not enter the 3rd phase of the moratorium.

Budapest, 01.10.2021

Yours sincerely,

UniCredit Bank Hungary Zrt.

Dear Client,

According to applicable laws, the payment moratorium will continue automatically and with unchanged terms until 30 September 2021 to clients who already have loans disbursed until that date under contracts existing on 18 March 2020. These are regulated by Act CVII of 2020 on transitional measures for the stabilization of the situation of certain priority social groups and enterprises in financial difficulty and Government Decree 637/2020 (XII. 22.) on the introduction of special emergency rules for the moratorium on loan payments.

Clients covered by the moratorium on 31 December 2020 will automatically be entitled to step into the second phase from 1 January 2021, this means that there is no need to apply for moratorium separately or confirm one’s eligibility.

However, debtors who did not avail themselves of the payment moratorium in December 2020, i.e. have previously opted out of it, but wish to use it in 2021, must notify their bank in writing, by post or via the bank’s standard electronic channel. The same applies to those whose last repayment instalment of 2020 was due before December, provided that they did not avail themselves of payment moratorium on such due date by previously opting out of it, but wish to avail themselves of it in 2021.

Please note that private individual clients do not need to submit proof of belonging to priority social groups in this case either.

25 June 2021

Kind regards,

UniCredit Bank Hungary Zrt.

Information for private individuals

Information for corporate clients

The payment moratorium will continue only to loans disbursed under credit agreements that were concluded and disbursed until 18 March 2020 and are still in force.

The loan payment moratorium has no impact on the right of companies under moratorium to perform their obligations according to the original terms and conditions; accordingly, you may still unilaterally declare your intention to opt out of the moratorium.

You can withdraw your unilateral opt-out declaration at any time until 30 September 2021, thereby opting back into the moratorium. Withdrawal of your declaration can be done by free-form mail by post or via the Internet banking system.

Modification of the payment dates of loan agreements under moratorium also modifies the ancillary and non-ancillary collaterals securing the loan agreement under the Hungarian laws (such as the contract of pledge, suretyship contract, guaranty contract, declaration of guaranty), regardless of whether the ancillary obligation has been executed as a contract or as a unilateral juridical act by the parties. Notarial deeds are not required to be modified.

If you have any questions about the moratorium, please reach out to your referent person.

We are updating our notices with the latest and most important information to know about the payment moratorium on a regular basis.

Learn more about our temporary relief measures introduced in lending to alleviate the negative impact of the COVID-19 pandemic.

25 June 2021

Kind regards,

UniCredit Bank Hungary Zrt.